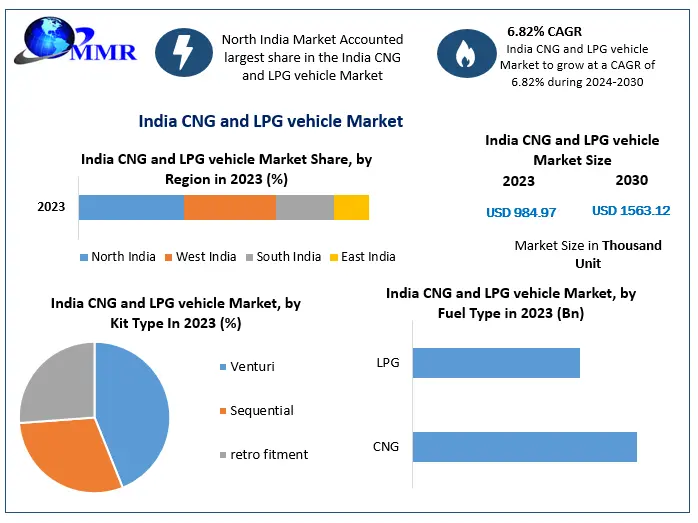

The India CNG and LPG Vehicle Market was valued at 984.97 thousand units in 2023 and is projected to grow at a CAGR of 6.82% from 2024 to 2030, reaching nearly 1,563.12 thousand units by 2030. Rising fuel costs, environmental concerns, and strong policy support are key factors accelerating the adoption of alternative fuel vehicles across the country.

Market Overview

CNG (Compressed Natural Gas) and LPG (Liquefied Petroleum Gas) vehicles have emerged as practical alternatives to conventional petrol and diesel vehicles in India. These vehicles offer lower emissions, reduced running costs, and improved fuel efficiency, making them increasingly attractive to both individual consumers and commercial operators.

The growing demand for cleaner mobility solutions, coupled with expanding fuel infrastructure, is reshaping the automotive landscape. Government initiatives, subsidies, and tax benefits are further encouraging automakers to expand their CNG and LPG vehicle portfolios.

India’s CNG infrastructure is rapidly expanding, with the number of stations expected to increase significantly—from around 3,900 stations across 236 cities in 2022 to over 10,000 stations in more than 300 cities by 2026—creating a strong foundation for market growth.

Request a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/20201/

Market Dynamics

Government Policies Driving Adoption

The Indian government is actively promoting the transition toward low-emission fuels. Policies encouraging the replacement of diesel engines with CNG and LPG systems in BS-VI compliant vehicles are playing a crucial role in market expansion.

CNG is considered an environmentally friendly fuel, emitting significantly lower levels of carbon monoxide, hydrocarbons, and particulate matter compared to traditional fuels. Regulatory support, combined with type-approval standards for retrofitting kits, is accelerating adoption across vehicle segments.

Rising Fuel Prices Boost Demand

The increasing cost of petrol and diesel is a major driver for CNG and LPG vehicle adoption. These alternative fuels offer substantial savings in operating costs, especially for high-usage vehicle owners such as fleet operators and commercial drivers.

Although the initial investment for CNG or LPG vehicles may be higher, users often recover the cost within a few years through fuel savings. This economic advantage continues to influence consumer preference toward gas-powered vehicles.

Challenges Impacting Market Growth

Despite strong growth prospects, the market faces certain challenges:

- Volatility in natural gas prices can directly impact demand. Significant price hikes have previously led to temporary declines in vehicle sales.

- Technical limitations, such as improper installation of kits and issues like inadequate drainage systems, may affect cylinder safety and durability.

- Limited refueling infrastructure in certain regions still requires route planning, which can discourage adoption in less-developed areas.

Segment Analysis

By Vehicle Type

The market is segmented into passenger vehicles and commercial vehicles.

Passenger vehicles dominate the market, driven by increasing consumer demand and strong offerings from leading automakers. Affordable CNG variants across hatchbacks, sedans, and compact MPVs are contributing significantly to segment growth.

By Fuel Type

Between CNG and LPG, CNG vehicles are expected to hold the largest market share by 2030. This dominance is attributed to:

- Lower fuel costs compared to petrol and diesel

- Better fuel efficiency

- Wider availability of CNG infrastructure

LPG vehicles, while present, have relatively lower penetration due to limited infrastructure and awareness.

By Kit Type

The market includes venturi kits, sequential kits, and retrofitment kits.

The retrofitment kit segment is projected to witness the fastest growth, supported by government initiatives allowing conversion of petrol vehicles to CNG under BS-VI norms. These kits offer improved fuel efficiency and reduced emissions, making them a preferred option among cost-conscious consumers.

Request a Free Sample Copy or View Report Summary:https://www.maximizemarketresearch.com/request-sample/20201/

Regional Insights

CNG vehicle adoption in India is highly concentrated in states such as Delhi, Haryana, Uttar Pradesh, Gujarat, and Maharashtra, where infrastructure and policy support are strong.

The expansion of the City Gas Distribution (CGD) network is expected to further boost adoption nationwide. Increasing availability of refueling stations and improved accessibility are key factors encouraging market penetration.

Government initiatives aim to significantly increase the share of natural gas vehicles by 2030, potentially reducing crude oil imports and enhancing energy security. This transition could also generate substantial economic benefits, including job creation and reduced environmental impact.

Competitive Landscape

The India CNG and LPG vehicle market is highly competitive, with leading automotive manufacturers expanding their alternative fuel vehicle offerings.

Key players include:

- Maruti Suzuki India

- Hyundai Motor India

- Tata Motors

- Toyota Motor Corporation

- Mahindra & Mahindra

- Honda Motor Company

- Ford Motor Company

- Volkswagen

- Mercedes-Benz

- Ashok Leyland

- Eicher Motors

- Volvo Group

Among these, Maruti Suzuki India remains a dominant player in the CNG passenger vehicle segment, offering a wide range of factory-fitted CNG models.

Future Outlook

The future of the India CNG and LPG vehicle market looks promising, supported by strong policy backing, infrastructure expansion, and increasing consumer awareness. Technological advancements in fuel storage, engine efficiency, and safety systems are expected to address existing challenges.

As India moves toward cleaner mobility solutions, CNG and LPG vehicles are poised to play a crucial transitional role before the widespread adoption of electric vehicles.

Conclusion

The India CNG and LPG vehicle market is set for steady growth over the forecast period, driven by cost advantages, environmental benefits, and supportive government initiatives. While challenges such as price volatility and infrastructure gaps remain, ongoing developments in technology and policy are expected to strengthen market adoption.

With increasing focus on sustainable transportation and reduced dependence on fossil fuels, CNG and LPG vehicles will continue to be a key component of India’s evolving mobility ecosystem.